In the world of finance and personal budgeting, understanding the various forms of credit available can empower individuals to make informed decisions about their money. One such option, the personal line of credit, has gained significant traction among borrowers looking for flexibility and convenience. This article delves into the intricacies of personal lines of credit, shedding light on how they function, their advantages and disadvantages, and tips for managing them effectively.

A personal line of credit offers a unique blend of features that can make it an appealing choice for many. Unlike a traditional loan, it provides access to a predetermined amount of money that can be borrowed, repaid, and borrowed again as needed. This revolving credit allows borrowers to only pay interest on the amount utilized, rather than the entire credit limit, thus potentially reducing overall borrowing costs.

Ultimately, when considering a personal line of credit, it’s vital to evaluate one’s financial needs, capacity to repay, and how this type of credit fits into their broader financial goals. With a deeper understanding of personal lines of credit, individuals can harness this tool to navigate financial challenges more adeptly.

Key Characteristics of a Personal Line of Credit

A personal line of credit is a flexible borrowing option that allows individuals to access funds as needed, making it particularly useful for unexpected expenses or larger purchases. It empowers borrowers to withdraw money up to a certain limit, repay it, and then draw on it again, much like a credit card. This adaptability distinguishes it from traditional loans, where the entire sum is made available upfront. The characteristics of personal lines of credit can influence how individuals manage their financial obligations and expenses.

- Revolving credit system

- Only pay interest on the amount borrowed

- Flexibility in borrowing and repayment

- Lower interest rates than credit cards

- Possible annual fees or maintenance charges

Understanding these key characteristics can help borrowers utilize a personal line of credit effectively, enabling them to navigate financial needs with more confidence and control.

How Do Personal Lines of Credit Work?

Personal lines of credit function similarly to credit cards, offering a pool of money that individuals can access at their discretion. After being approved for a credit limit by a lender, the borrower can withdraw any amount from that limit. The crucial aspect to note is that interest is only charged on the amount withdrawn, allowing for potentially lower costs compared to other forms of borrowing.

Repayment of a personal line of credit occurs in a flexible manner, with borrowers typically making monthly payments that cover interest and some principal. Depending on the lender's terms, there may be options to make larger payments or pay off the entire balance at any time without penalties, enhancing the appeal of this borrowing method.

Types of Personal Lines of Credit

There are two primary types of personal lines of credit available, each catering to different financial needs and circumstances. By understanding these categories, borrowers can make better decisions aligned with their financial strategies. The distinctions between unsecured and secured lines of credit play a crucial role in determining interest rates, borrowing limits, and risk factors involved in borrowing.

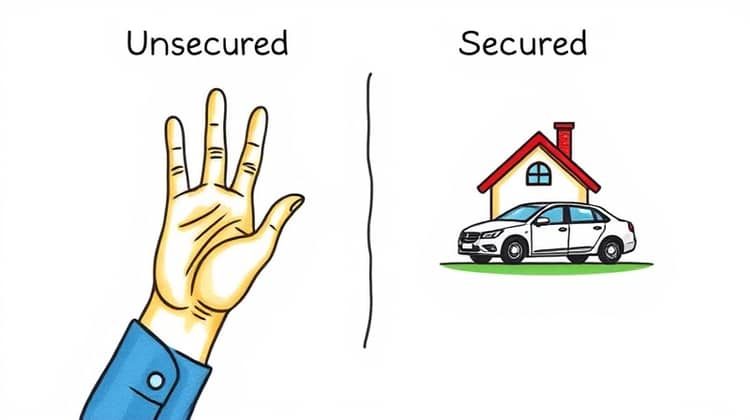

An unsecured line of credit does not require any collateral, making it a more accessible option for individuals without assets to pledge. Conversely, a secured line of credit necessitates the backing of an asset, such as a home or car, which can lead to lower interest rates but also introduces a higher risk factor for the borrower. Both types have their pros and cons that users need to consider in relation to their particular needs.

- Unsecured Lines of Credit

- Secured Lines of Credit

The choice between an unsecured line of credit and a secured line of credit can significantly impact a borrower’s financial journey, influencing their ability to access funds and manage debt effectively.

1. Unsecured Lines of Credit

Unsecured lines of credit are often more appealing to individuals who may not have adequate collateral to secure a loan. They function based on the borrower’s creditworthiness, which is evaluated by credit score and financial history. As such, they tend to have higher interest rates compared to secured lines of credit due to the lack of collateral that the lender can claim in case of default.

Aside from interest rates, unsecured lines of credit also typically come with lower credit limits than their secured counterparts. Borrowers should weigh the costs against their financial needs to determine if an unsecured line aligns with their objectives, especially when dealing with larger expenses or emergencies.

2. Secured Lines of Credit

Secured lines of credit provide borrowers the advantage of accessing larger credit limits and lower interest rates. Since they require collateral, lenders have a safety net that reduces their risk, which translates into better terms for borrowers. This makes secured lines an attractive option for individuals planning significant expenditures or consolidating existing debts.

Nonetheless, locking in an asset as collateral carries inherent risks. If a borrower fails to meet repayment obligations, they risk losing the asset used to secure the line of credit. Thus, it’s essential for individuals to consider their financial stability and repayment capability before committing to a secured line of credit.

- Lower interest rates than unsecured lines

- Higher credit limits available

- Better terms and repayment options compared to unsecured lines

Choosing between an unsecured and secured line of credit requires careful consideration of the borrower's financial stability, needs, and potential risks involved.

Advantages of Personal Lines of Credit

Personal lines of credit come with various advantages that can significantly benefit borrowers, depending on their unique financial situations. One of the primary benefits is the flexibility they offer; individuals can withdraw funds as needed, making it ideal for unexpected expenses or cash flow management. This flexibility also means that borrowers only pay interest on the amount they use, rather than the total credit limit available.

Moreover, personal lines of credit often feature lower interest rates compared to credit cards, which can lead to considerable savings over time for those who manage their debt responsibly. They can also enhance one’s credit score when used judiciously, as they contribute to credit mix and overall credit utilization ratios.

- Access to funds when needed

- Lower interest rates compared to credit cards

- No interest charged on unused credit

- Improvement of credit history with responsible use

These advantages make personal lines of credit a compelling option for many borrowers looking for financial flexibility and cost-efficiency.

Disadvantages of Personal Lines of Credit

While personal lines of credit offer numerous benefits, they also come with specific disadvantages that potential borrowers must consider. One concern is the potential for accumulating debt. Since they provide fluid access to funds, individuals can be tempted to borrow excessively, which can lead to financial trouble if not managed properly. It's crucial to have a clear repayment plan to avoid falling into a cycle of debt.

Interest rates can also vary widely, particularly for unsecured lines of credit. Borrowers with lower credit scores may face significantly higher rates, making borrowing less affordable. Moreover, if borrowers fail to make timely payments, they risk damaging their credit scores and incurring additional fees, which can compound financial strain.

- Potential for excessive borrowing and debt accumulation

- Variable interest rates can increase costs

- Risk to credit scores with missed payments and defaults

- Possible annual fees and maintenance costs

Understanding these disadvantages can help borrowers navigate their finances wisely and develop strategies to avoid costly mistakes when utilizing personal lines of credit.

How to Apply for a Personal Line of Credit

When considering applying for a personal line of credit, potential borrowers should prepare by reviewing their credit reports and assessing their financial situation. Most lenders will evaluate the applicant's credit score, income, and debt-to-income ratio, so ensuring these elements are in good standing can enhance the chances of approval.

Once ready to apply, borrowers should research different lenders to compare terms, interest rates, and potential fees that may apply. Gathering necessary documents, such as proof of income and existing debts, will streamline the process and provide lenders with a clearer picture of the applicant's financial standing.

- Check and understand your credit report

- Assess your financial situation and needs

- Research potential lenders and compare their offerings

- Gather necessary documentation for the application

By following these steps, borrowers can improve their chances of approval and secure favorable terms for their personal line of credit.

Tips for Managing a Personal Line of Credit

Managing a personal line of credit efficiently is essential to prevent any potential pitfalls and to maximize its benefits. Establishing a clear budget and sticking to it can help minimize the risk of borrowing excessively and incurring unnecessary debt. It’s crucial to treat the line of credit like any other loan, ensuring that repayments are prioritized to avoid fees and penalties.

- Create and follow a budget to limit borrowing

- Pay the full balance whenever possible

- Make payments on time to maintain a good credit score

- Regularly review your credit utilization to stay on track

By implementing these managing tips, borrowers can enhance their financial health and ensure that their personal line of credit serves as a valuable asset rather than a burden.

Conclusion

In summary, personal lines of credit can offer significant benefits to borrowers seeking financial flexibility and support for modern-day expenses. Their unique structure, allowing for revolving credit and payment only on the amount borrowed, makes them an attractive alternative to traditional loans and credit cards. However, potential borrowers must take the time to understand how personal lines of credit work, the types available, and the implications of their use.

By weighing the advantages and disadvantages carefully, individuals can make informed choices that align with their financial goals. Responsible management and a clear repayment plan are critical to ensure that a personal line of credit enhances financial stability rather than detracts from it.

In conclusion, as with any financial product, it is crucial to do thorough research and consider personal circumstances before committing to a personal line of credit. Being informed and proactive can pave the way for sound financial decision-making and a healthier financial future.