In recent years, peer-to-peer (P2P) lending has gained immense popularity as an alternative financing option for borrowers and investors alike. This innovative model leverages technology to eliminate traditional financial institutions from the lending process, creating a more direct and often more accessible way for individuals to obtain loans. As the financial landscape evolves, it is essential to understand the nuances of P2P lending to determine if it is the right fit for your needs.

This article will delve into what peer-to-peer lending entails, how it functions, its potential advantages and risks, and who might benefit from this alternative financing model. By the end, readers will have a comprehensive understanding of P2P lending and its implications for both borrowers and investors. Whether you are looking to borrow money quickly or seeking new investment opportunities, P2P lending may offer solutions worth considering.

What Is Peer-to-Peer Lending?

Peer-to-peer lending, often abbreviated as P2P lending, is a method of borrowing and lending money directly between individuals through online platforms. This approach allows borrowers to access funds from individual investors, bypassing traditional banks or financial institutions. By utilizing an online platform, P2P lending has reinvented the lending process, making it faster, more convenient, and potentially more affordable for those involved.

The concept of P2P lending emerged in the early 2000s and has since grown significantly, driven by technological advancements and a changing economic landscape. It offers borrowers an alternative to traditional loans with varying terms, interest rates, and repayment schedules. Investors, on the other hand, can diversify their portfolios and potentially earn higher returns compared to traditional savings accounts or fixed-income investments.

In essence, peer-to-peer lending fosters a marketplace where borrowers and investors connect, negotiate terms, and execute transactions directly without intermediary banks.

How Does P2P Lending Work?

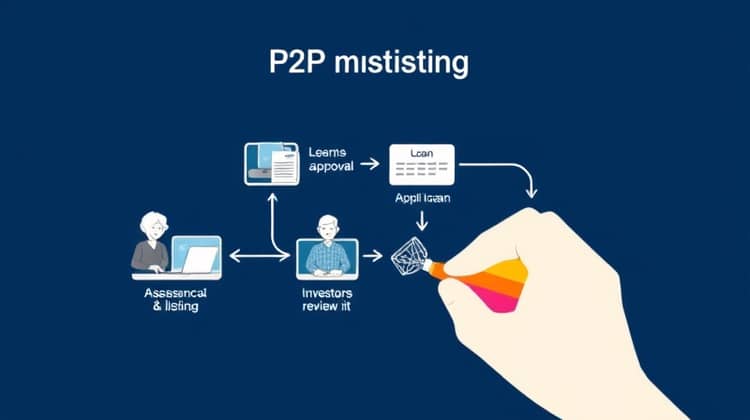

The P2P lending process typically begins with a borrower submitting a loan application on a P2P platform. This application usually includes details about the amount requested, purpose of the loan, and an outline of the borrower’s financial history. Once a borrower applies, their creditworthiness is assessed through a variety of means, including credit scores and financial background checks. Based on this assessment, the platform will assign an interest rate to the loan, reflecting the associated risk.

After the loan is approved and listed on the platform, investors can review the loan request and choose to fund all or part of the loan amount. Once the required financing is secured, the loan is disbursed to the borrower, who will then begin repaying it over an agreed-upon term. Investors receive monthly payments of principal and interest, providing a potential income stream.

Advantages of Peer-to-Peer Lending

One of the primary advantages of P2P lending is accessibility. Borrowers who may struggle to obtain loans from banks due to stringent credit requirements can often find favorable terms through P2P platforms. This opens opportunities for individuals with varying credit profiles, including those with less-than-perfect credit histories.

Additionally, P2P lending can offer lower interest rates compared to traditional loans. Since P2P platforms operate with lower overhead costs than banks, they often pass some of these savings on to borrowers in the form of reduced interest rates. As a result, borrowers can potentially save money over the life of their loans. Understanding these aspects can aid in making informed financial decisions.

- Access to a wider range of potential investors

- Possibility of lower interest rates

- Flexibility in loan terms

While P2P lending presents numerous advantages, potential borrowers and investors should carefully evaluate their own situations before engaging with this model.

Potential Risks and Challenges

Despite its advantages, peer-to-peer lending carries certain risks that participants should be aware of. One significant concern is the possibility of borrower default, which could result in lost funds for investors. Unlike traditional banks, P2P platforms are not insured by government entities, meaning investors bear the full risk if borrowers fail to repay their loans. Therefore, proper due diligence is essential when choosing which loans to fund to mitigate this risk.

Furthermore, the P2P lending landscape is still relatively new and may be subject to regulatory changes that could impact its operation. Potential investors should remain informed about the development of regulations surrounding P2P lending, as these changes could affect the security and stability of their investments.

- Risk of borrower defaults

- Regulatory uncertainty

- Limited recourse options for investors

Recognizing these challenges allows individuals to make more educated choices when considering P2P lending opportunities.

Who Should Consider P2P Lending?

Peer-to-peer lending can be suitable for various individuals, including both borrowers in need of funds and investors seeking returns. Specifically, those who may benefit from P2P lending include:

- Borrowers who struggle to secure traditional loans

- Investors looking for alternative investment opportunities

- Individuals who prefer direct transactions rather than going through banks

It is essential for both parties to evaluate their financial health and risk tolerance before participating in P2P lending.

How to Get Started with P2P Lending

To engage in P2P lending, individuals can follow these initial steps:

- Research and choose a reputable P2P lending platform.

- Create an account and complete the necessary verification processes.

- If borrowing, submit a loan application. If investing, browse available loans to fund.

Taking these steps can help individuals successfully navigate the P2P lending landscape and capitalize on available opportunities.

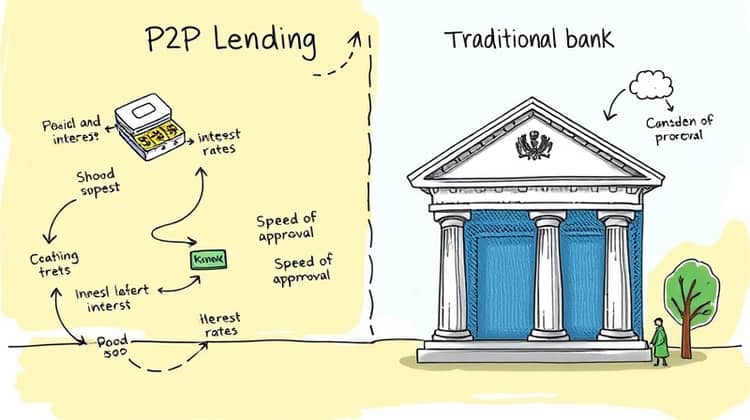

P2P Lending vs. Traditional Loans

When considering financing options, it's important to understand the key differences between peer-to-peer lending and traditional loans:

- P2P lending typically has more flexible eligibility criteria compared to banks.

- Interest rates on P2P loans may be lower than those offered by traditional lenders.

- Loan approval processes in P2P lending can often be faster and more streamlined.

Understanding these distinctions enables borrowers and investors to make more strategic financial decisions.

Conclusion

Peer-to-peer lending presents a new frontier in the lending marketplace, connecting borrowers and investors directly through innovative technology. As this model continues to grow, understanding its mechanics, advantages, and risks becomes increasingly important for participants. By taking the time to explore P2P lending and its implications, individuals can better position themselves to make informed financial decisions that align with their goals.

Ultimately, whether or not P2P lending is the right option for you will depend on your personal financial circumstances and goals. For those willing to engage with this model carefully and responsibly, peer-to-peer lending can provide an alternative path to obtaining funds or generating returns.