In today's world, healthcare costs are skyrocketing, making it increasingly difficult for patients to afford necessary medical treatments. With the rise of various financing options, medical loans have emerged as a solution for individuals facing unexpected medical expenses. These loans can cover everything from medical bills to elective surgeries, allowing patients to focus on their recovery without the burden of financial stress.

Understanding medical loans involves recognizing the specific terms, conditions, and requirements that define them. This form of borrowing is designed to help individuals manage the costs associated with healthcare, which may often come as a surprise. Additionally, medical loans can vary significantly from traditional personal loans, as they often take into account the nature of health care services and the urgency of medical needs.

As you navigate your options for financing medical expenses, it's vital to grasp the different types of loans available, the factors that could affect your decision, and alternative funding options. By doing so, you will be better equipped to make informed choices regarding your healthcare financing.

Understanding Medical Loans

Medical loans are specifically tailored financial products aimed at helping individuals pay for healthcare-related expenses. Unlike typical personal loans, medical loans can encompass various types of medical services, from major surgeries to outpatient procedures. These loans provide patients with a way to manage large medical bills that they may not have immediate and adequate resources to pay.

One noteworthy aspect of medical loans is that they may come with flexible repayment terms. Many lenders recognize the financial burden that can accompany healthcare costs and, consequently, offer flexible payment plans, low-interest rates, or even deferred payment options. This makes medical loans an appealing choice for many patients, particularly those who might face extensive medical procedures or treatments.

Additionally, obtaining a medical loan often involves a straightforward application process, allowing patients to access the necessary funds quickly, right when they need them the most. This accessibility is crucial, especially in emergency situations where timely treatment might be paramount to a favorable outcome.

Types of Loans for Medical Expenses

Various types of loans are available to assist with medical expenses, each designed to cater to specific financial needs.

- Personal Loans

- Medical Credit Cards

- Patient Financing Plans

- Home Equity Loans

- Short-Term Loans

Each of these loan types offers distinct advantages and can be tailored to fit your situation, ensuring you receive the care you need without the financial strain.

Factors to Consider Before Taking a Medical Loan

Before committing to a medical loan, it's crucial to evaluate several key factors that can impact your long-term financial situation. For one, consider the interest rates and fees associated with the loan. Higher interest rates can significantly increase the total cost of borrowing, making it essential to shop around for the best deals. Understanding the full financial implication of a loan is vital before moving forward.

Secondly, assess your ability to repay the loan on time. Since a medical loan could stretch across several months or years, ensure that your budget allows for regular payments. Skipping payments may lead to additional charges and negatively affect your credit score, thus compounding your financial challenges.

- Interest Rates and Fees

- Loan Terms

- Your Credit Score

- Repayment Options

- Borrower Protections

Thoroughly reviewing these factors ensures that you take a well-informed approach to financing your medical expenses.

Alternative Funding Options

While medical loans can be a viable option for covering healthcare costs, it is also prudent to explore alternative funding solutions that may be available. Some individuals may want to consider negotiating directly with healthcare providers for reduced rates or payment plans, as many hospitals and clinics are open to working with patients to make healthcare more affordable. Moreover, there are organizations and charities dedicated to providing financial assistance for medical care, particularly for those facing severe financial hardships.

Additionally, leveraging health savings accounts (HSAs) or flexible spending accounts (FSAs) can also provide significant pre-tax savings which can offset medical expenses. By utilizing these accounts, individuals can access funds that are specifically set aside for medical expenses, often resulting in tax advantages.

- Negotiate with Healthcare Providers

- Seek Financial Assistance from Charities

- Use Health Savings Accounts (HSAs)

- Explore Flexible Spending Accounts (FSAs)

By considering these alternatives, individuals may find more manageable ways to afford the medical care they need.

How to Apply for a Medical Loan

The process of applying for a medical loan can be relatively straightforward if you know the steps involved. Initially, it is essential to assess your financial needs and gather all relevant documentation, including income statements, existing debt obligations, and medical bills. Having these documents in order can streamline the application process and enhances your chances of approval.

Next, research various lenders that offer medical loans, comparing interest rates, fees, and repayment options. Once you have chosen a lender, proceed with filling out the application form, securely submitting your financial information.

- Research Lenders

- Gather Personal and Financial Documents

- Complete the Application Form

- Provide Additional Information If Required

- Review Loan Terms Before Signing

Finalizing your loan application with thoughtful consideration of the terms and conditions is essential to avoid any hidden fees or misunderstandings later.

Costs Associated with Medical Loans

It's imperative to understand the costs tied to medical loans beyond just the principal amount borrowed. First and foremost, interest rates represent a significant component of the overall cost of the loan, varying widely based on creditworthiness and lender policies.

Furthermore, potential fees can arise, such as origination fees, late payment fees, and prepayment penalties. Each of these associated costs can contribute to a higher financial burden, making it crucial for borrowers to review all terms before proceeding.

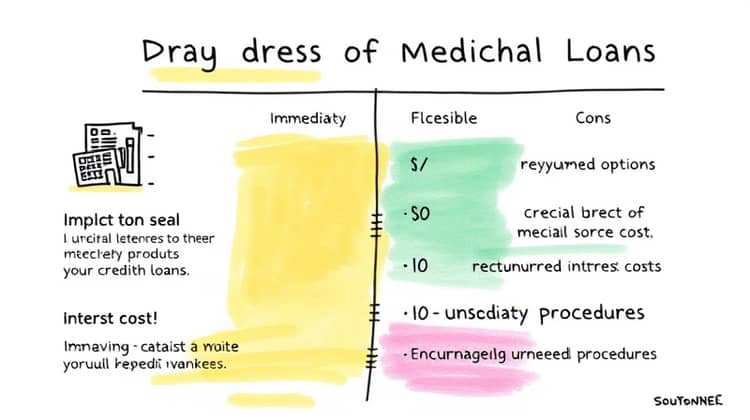

Pros and Cons of Loans for Medical Expenses

Like any form of borrowing, medical loans come with a range of pros and cons that should be weighed before making a decision. On the positive side, medical loans can assist in covering large medical expenses and help patients receive necessary treatment without extensive waiting times.

Conversely, accumulating debt can lead to financial strain, particularly if borrowers find themselves unable to keep up with payments.

- Immediate Access to Funds

- Flexible Repayment Options

- Potential Impact on Credit Score

- Accrued Interest Costs

- May Encourage Unneeded Procedures

Understanding these advantages and potential downsides is essential in determining whether a medical loan is the right option for you.

Conclusion

In conclusion, medical loans serve as an important financial tool for individuals facing expensive healthcare needs. While they can provide quick access to funds and facilitate timely treatment, borrowers must carefully consider the terms and their ability to repay before committing to a loan.

Additionally, exploring alternative funding options and understanding the various costs involved in medical loans can empower individuals to make informed choices. It's essential to weigh the pros and cons and to assess your financial situation adequately.

Ultimately, the decision to take a medical loan should be made with careful consideration, always keeping in mind the importance of your health and financial well-being.