In today's financial climate, many individuals and families are exploring various lending options to support their needs and aspirations. One often-overlooked option is credit unions, which offer a range of loan products with distinctive advantages compared to traditional banks. This article delves into the benefits of credit union loans and provides a guide on how to apply for them effectively.

Whether you're considering a personal loan, auto loan, or home equity line of credit, understanding credit unions can help you make informed financial decisions. Let's take a closer look at what credit unions are and the unique benefits they bring to their members.

What is a Credit Union?

Credit unions are member-owned financial cooperatives that provide a variety of financial services, including loans, savings accounts, and other banking solutions. Unlike traditional banks, which are profit-driven institutions, credit unions focus on serving their members' financial needs. This model promotes a strong sense of community and often results in more personalized service for customers.

Members of a credit union pool their resources, allowing the institution to offer more favorable interest rates and terms on loans and deposits. Joining a credit union typically requires meeting certain membership criteria, which can be based on geographic location, employer affiliation, or membership in a particular organization.

The Benefits of Credit Union Loans

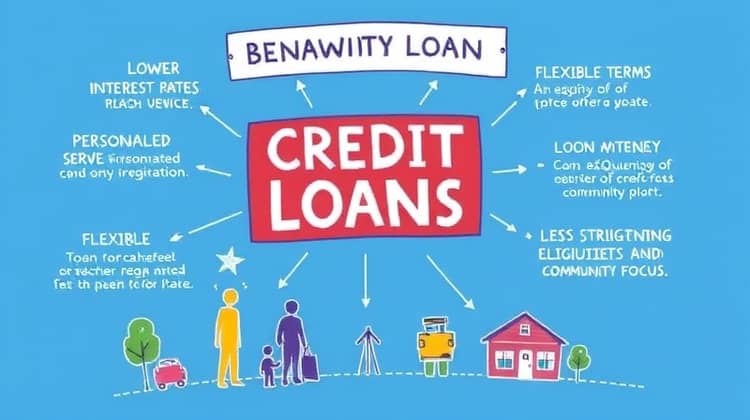

Credit unions offer significant advantages over traditional banks when it comes to securing loans. Their member-centric approach means that they prioritize the needs of the borrowers, often resulting in lower rates and more flexible terms. Understanding these benefits can help you decide if a credit union loan is the right choice for you.

One of the biggest draws of credit union loans is their competitive interest rates, which can save borrowers a substantial amount of money in repayments over time. Let's explore the key benefits in detail.

- Lower Interest Rates

- Personalized Service

- Flexible Terms

- Less Stringent Eligibility Requirements

- Community Focused

These benefits highlight why many individuals choose to pursue loans from credit unions over traditional banking options. Let's take a closer look at each of these advantages.

1. Lower Interest Rates

One of the primary advantages of credit union loans is the lower interest rates they often offer compared to banks. Since credit unions are nonprofit organizations, they can pass on savings from reduced overhead costs directly to their members through more favorable loan terms.

This means that the effective cost of borrowing is usually much lower for credit union members, which can be particularly beneficial when taking out larger loans, such as mortgages or auto loans. Borrowers can potentially save thousands of dollars in interest payments throughout the loan's life.

- Credit unions typically offer lower APRs than banks.

- They provide attractive rates for various types of loans, including personal, auto, and home loans.

- Members may also benefit from lower fees in addition to lower interest rates.

In summary, lower interest rates are a significant advantage for anyone considering a loan from a credit union, making repayment more manageable and cost-effective.

2. Personalized Service

Credit unions pride themselves on offering personalized service that tailors to the individual needs of their members. This customer-focused approach stems from their community-oriented mission and the understanding that each member's financial situation is unique.

With fewer bureaucratic layers than larger banks, credit union staff can take the time to understand each member’s needs, goals, and circumstances. This often leads to customized loan products that fit better into the borrower’s financial plan.

In addition, credit unions typically foster a friendly, supportive environment, making members feel comfortable discussing their financial needs and challenges.

3. Flexible Terms

Credit unions often have more flexible loan terms compared to traditional banks, which can accommodate a wider variety of financial situations. For example, credit unions may allow for extended repayment periods or custom payment plans that take into account members' income cycles or financial goals.

This flexibility can be particularly beneficial for members who may have non-traditional sources of income or those who are looking to borrow for unique circumstances.

- Extended repayment terms can be negotiated depending on the loan type.

- Members may request adjustments to repayment schedules if they face financial hardship.

- Credit unions can provide alternative collateral options for secured loans.

This adaptability in terms is a critical advantage for borrowers, helping to alleviate stress and improve the overall lending experience.

4. Less Stringent Eligibility Requirements

Credit unions often have less stringent eligibility requirements than traditional banks. This can be particularly advantageous for individuals with less-than-perfect credit scores or those who are new to the credit market.

Due to their focus on serving members within specific communities or groups, credit unions may offer a more approachable lending process that considers the overall financial picture rather than just a credit score.

5. Community Focused

Credit unions have a strong community focus, often working closely with their members to foster financial well-being within the community. This means that they are more likely to invest in local initiatives and support businesses and nonprofits.

By choosing a credit union for your loan, you're not just benefiting from better loan terms; you're also helping contribute to the economic health of your community.

Types of Loans Offered by Credit Unions

Credit unions provide a diverse range of loan options to meet the different needs of their members. These can include personal loans, auto loans, home mortgages, and credit lines.

Additionally, many credit unions have specialized programs designed to help members with specific financial goals, such as starting a business or funding education.

Understanding the variety of loans available can help you select the right product that fits your financial needs.

- Personal loans

- Auto loans

- Home loans

- Credit cards

- Business loans

This diverse loan product offering ensures that members have access to just about any funding solution they may require.

How to Apply for a Loan from a Credit Union?

Applying for a loan from a credit union can be a simple and straightforward process. However, it is essential to approach it methodically to ensure a successful application experience. Knowing the steps involved can help streamline the process and improve your chances of approval.

Let's explore the essential steps to consider when applying for a credit union loan.

1. Research Various Credit Unions

The first step in applying for a credit union loan is to research the various credit unions available to you. Each credit union has its own membership requirements, loan products, and interest rates, so it's vital to compare these factors.

Identify credit unions that align with your financial needs and explore their offerings thoroughly to find the best fit before proceeding with an application.

2. Check Membership Requirements

After narrowing down your options, check the membership requirements for the credit unions you are interested in. Many credit unions have specific eligibility criteria that you must meet to become a member, such as residency in a particular area or employment with specific companies.

3. Gather Necessary Documentation

Before submitting your application, gather all necessary documentation to support your loan request. This paperwork can greatly influence your chances of approval and may include proof of identity, income verification, and details about your financial history.

Consider compiling the following documents to enhance your application process:

- Identification documents (e.g., driver's license, passport)

- Proof of income (e.g., pay stubs, tax returns)

- Financial statements (e.g., bank statements, debt obligations)

- Purpose of the loan and budget plan

Being well-prepared with the right documents can help ensure your application process proceeds smoothly.

4. Submit Your Application

With your documentation ready, it's time to submit your application. Depending on the credit union, this can often be done online, in person, or even over the phone. Make sure that you fill out the application completely and accurately to prevent any delays in processing.

Some credit unions may also require an interview or additional discussion to clarify details about your application, so be prepared for that opportunity to express your financial needs.

5. Review the Loan Offer

Once your application has been processed, you will receive a loan offer from the credit union. It's crucial to review the terms and conditions of the offer carefully.

Examine the interest rates, repayment terms, and any additional fees or policies associated with the loan. If you have questions or concerns, don't hesitate to reach out to the credit union’s staff for clarification.

6. Accept the Loan Terms

If the loan offer aligns with your financial needs and expectations, it's time to accept the terms. This often involves signing a loan agreement that legally binds you to the outlined repayment conditions. Make sure you fully understand your responsibilities as a borrower before signing on the dotted line.

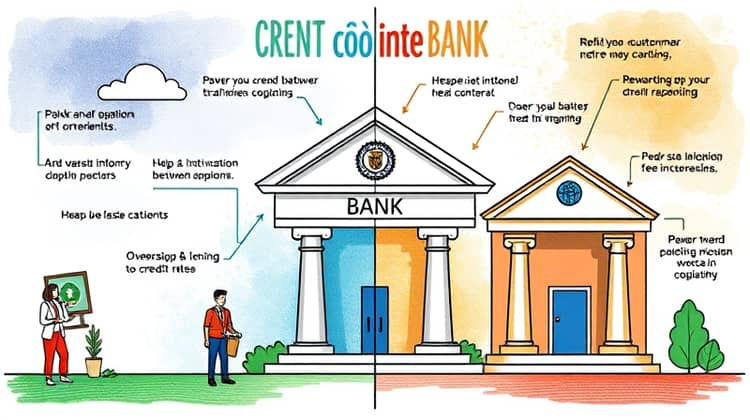

Key Differences Between Credit Unions and Banks

While both credit unions and banks offer similar services, significant differences set them apart. Credit unions operate as nonprofit entities and are owned by their members, while banks are for-profit institutions primarily focused on earnings for shareholders.

Moreover, credit unions tend to offer lower fees and interest rates, along with a more personalized customer service experience compared to larger banks, which may have a more transactional approach in their dealings with clients.

Conclusion

Credit union loans can be a smart and financially beneficial choice for borrowers seeking tailored, community-focused banking solutions. With their favorable terms, personalized service, and commitment to serving members, credit unions stand out as a viable alternative to traditional banking institutions.

Whether you're looking to borrow for personal purposes, a new vehicle, or a home, exploring loans from credit unions can lead you to more cost-effective and supportive lending options. Take the time to discover what a credit union can do for your financial future.